National Grid @ 639.5p, +1p (+0.16%)

I can't see too much upside on National Grid until the year-end results come through in May 2012 and even then I wouldn't expect anything spectacular unless it be related to the future direction of the company's US operations.

But, spectacular isn't the name of the game here!

What I would be looking for is: confirmation that capital investment plans are comfortably funded, signs that debt levels are being managed, and a strong link between earnings and inflation.

But, this post wasn't necessarily about looking forward. Instead it is more about looking at the performance of National Grid's shares to date.

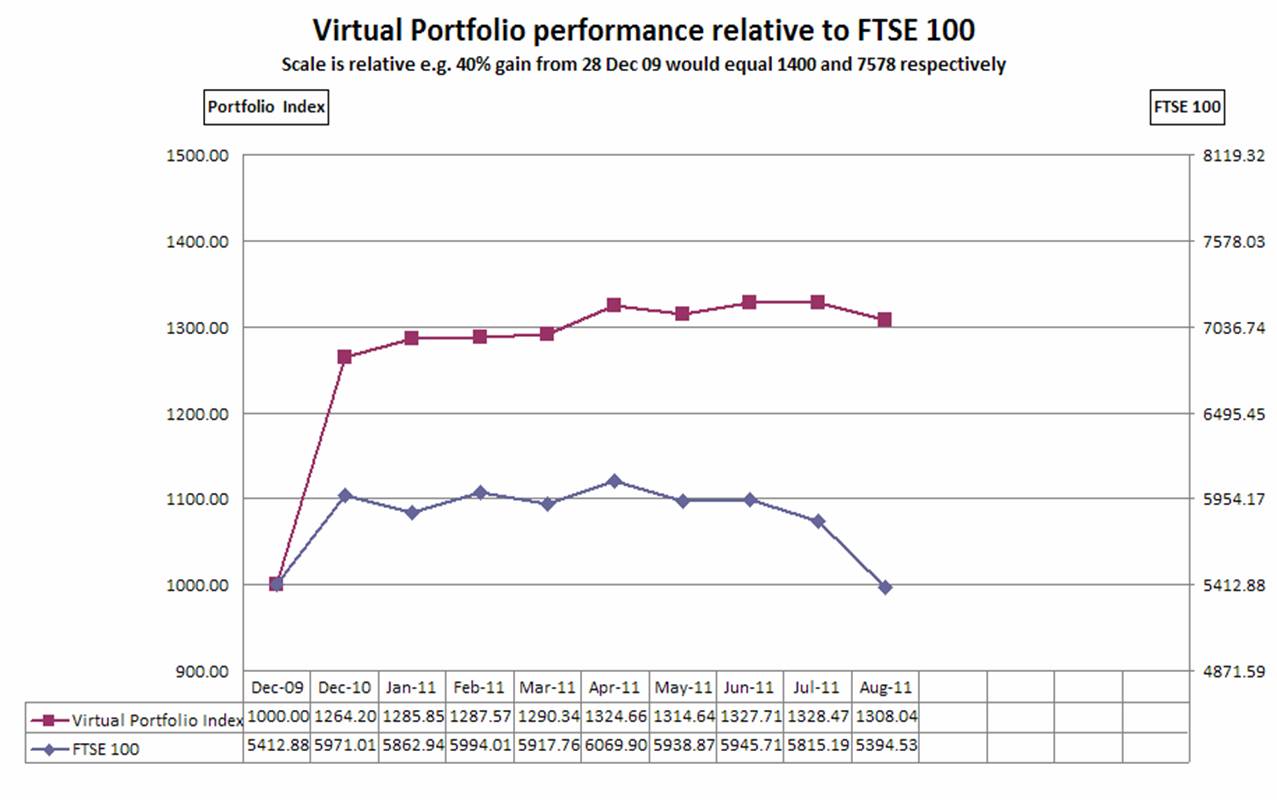

As it stands, the shares have performed very strongly in this recent period of volatility and pushed their intra-day 52 week high to 640p this morning.

640p represents a YTD gain of 15.73% against the FTSE 100 which, at 5351.63, is down by 10.73%.

Its worth noting that the FTSE's performance includes National Grid's gains in it but that its weighting in the index is insufficient to balance the sectors that have fallen back.

And then there is the dividend which has yielded a further 6.5% this year which, when added to the performance of the share price represents a total YTD gain of 22.23% v. the FTSE's -10.73%.

To be fair I haven't calculated a yield for the FTSE but it probably averages about 4% which would reduce the loss to -6.73%. Still, the difference between 22.23% and -6.73% is 28.96%!

A number of discussion points stand out here:

- the possible defensive qualities of National Grid as it operates as a virtual monopoly to the UK with its utility services infrastructure of transmission pipes and wires. As such this should give it unspectacular but steady revenues that are predictable within a narrow range.

I can't foresee a time that a competitive alternative could be planned, funded and, more importantly, be approved. The disruption and cost is too great and the political will is just not there.

- earnings linked to inflation. Being regulated gives it both advantages and disadvantages in terms of what it can charge but serves to smooth things out I feel. Inevitably, inflation is used as a benchmark so I would expect a strong link between earnings and inflation. Capital requirements are worth noting here as well as they are also taken into account by the regulator.

- some confidence that the dividend will be maintained given the previous points.

- the dividend itself, at a forecast 6.4%, is comfortably at the top-end of yields in the utility sectors (Scottish and Southern is 6.15% but United Utilities is 5.3%).

- the utility sector choice continues to diminish with Northumbrian Water the next to disappear given a recently accepted offer. This means less choice when there is a market flight to defensive sectors. Less choice means more premium when supply can't meet demand.

Finally, the performance of National Grid goes some way to demonstrating the possible virtues of diversification and some attempt at balance in a portfolio.

It may seem a bit boring and profit denting when markets are in their bull phase but I am currently very appreciative of the steadier, more defensive shares in the portfolio. National Grid has (currently) managed to balance some of my heavier losses with capital gains, and its dividend has helped to fund my hopefully, opportunistic purchases in the last couple of months.

The portfolio is far from perfect and will, no doubt, be hit hard should the market's fears become reality (from overreaction if nothing else).

I also expect that should the market begin to stabilise and recover, the "defensive" qualities of National Grid will be less in demand which will likely see the shares pull back from the current 52 week highs. But then I can always content myself with the dividend and the fact that any pull back is a consolidation of its YTD gains.

As ever, there is also a bit of caution required for possible surprises from the company. The most recent being last year's rights issue hence my looking for confirmation that capital investment plans are adequately funded.

What are my ambitions for National Grid?

Well, I reckon that from hereon in, if the shares could gain by 4.7% per annum and the company matches this with a similar increase to the dividend then this would give me a 100% gain by 2016 at which point it will also be yielding almost 8% against my original investment.

Is this too ambitious you might ask (or not ambitious enough?).

Well it might be, but the company has an intent to increase its dividend by 8% this year and next and, by virtue of it being in a regulated market, the company's earnings are linked to inflation (typically RPI less efficiency savings plus capital requirements).

At this point, I also appreciate that for many investors this isn't sufficiently attractive on its own but it is all about finding and balancing your own levels and expectations of risk and reward, and portfolio diversification means that I have other investments in which I have greater expectations.

Carry 4.7% forward again and I reckon that I could get my investment back a second time in just 5 years more, 2021 at which point the shares could be yielding over 10% against my original investment.

However, on a cautionary note, markets and share prices don't travel in straight lines but I will be keeping an interested eye on boring old National Grid!

Related posts:

-

August 2011: Portfolio Update.

-

National Grid Powers up: Interim Management Statement

-

National Grid preliminary results y/e 31 March 2011